Pure Mathematics

Vol.04 No.06(2014), Article ID:14392,6

pages

10.12677/PM.2014.46038

Asymptotic Properties for the Parameter Estimator in the Near-Explosive Autoregressive Process

Mingming Yu, Jiao Meng

Nanjing University of Aeronautics and Astronautics, Nanjing

Email: mengyilianmeng@163.com, zbmengjiao@sina.com

Received: Oct. 13th, 2014; revised: Nov. 11th, 2014; accepted: Nov. 20th, 2014

Copyright © 2014 by authors and Hans Publishers Inc.

This work is licensed under the Creative Commons Attribution International License (CC BY).

http://creativecommons.org/licenses/by/4.0/

ABSTRACT

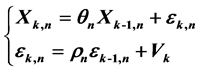

In this paper, we focus our attention on the following near-explosive autoregressive process: . When

. When  and

and  in the near-explosive case, the asymptotic distributions for the least squares estimator of

in the near-explosive case, the asymptotic distributions for the least squares estimator of  can be obtained.

can be obtained.

Keywords:Autoregressive Process, Least Squares Estimator, Near-Explosive

近爆炸性自回归序列中参数估计量的渐近性质

于明明,孟娇

南京航空航天大学,南京

Email: mengyilianmeng@163.com, zbmengjiao@sina.com

收稿日期:2014年10月13日;修回日期:2014年11月11日;录用日期:2014年11月20日

摘 要

本论文的目的是研究近爆炸性自回归序列 中, 当

中, 当 ,

, 时参数

时参数 最小二乘估计量的渐近分布。

最小二乘估计量的渐近分布。

关键词 :自回归序列,最小二乘法估计量,近爆炸

1. 介绍

本文我们讨论下面自回归序列:

. (1)

. (1)

并且满足下列假设:

(1) ,

, 是未知参数,并且满足

是未知参数,并且满足 ,

, ,

, ,其中

,其中 且

且 ;

;

(2) 是独立同分布

是独立同分布 随机变量,且

随机变量,且 ,

, ;

;

(3) 。

。

为了估计未知参数 ,我们通过使

,我们通过使 的值达到最小得到

的值达到最小得到 的最小二乘估计为

的最小二乘估计为 ,

, 。

。

首先,当 是一个固定的常数

是一个固定的常数 且

且 时,这种情况下

时,这种情况下 的渐近分布已经被很多科研者证明出来,我们可以参考文献 [1] [2] ,情况再复杂一点,当

的渐近分布已经被很多科研者证明出来,我们可以参考文献 [1] [2] ,情况再复杂一点,当 也是一个固定的常数

也是一个固定的常数 时,在 [3] 中,作者证出了

时,在 [3] 中,作者证出了 的渐近正态性。其次,科研者们不再满足于研究

的渐近正态性。其次,科研者们不再满足于研究 固定时的情况,假设

固定时的情况,假设 是一个可变的序列,

是一个可变的序列, ,Chan

,Chan

和Wei在 [4] 中证出了在 时,

时, 渐近于一个布朗运动,当

渐近于一个布朗运动,当 ,在 [5] 中,作者给出

,在 [5] 中,作者给出

了 的渐近分布。

的渐近分布。

最后,在这篇文章中我们来考虑 ,

, ,

, 时

时 的渐近性质。我们有如下主要的结论:

的渐近性质。我们有如下主要的结论:

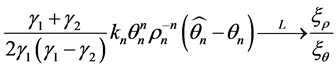

定理1:当 充分大时

充分大时

,

,

这里 表示依分布收敛,

表示依分布收敛, ,其中

,其中 。

。

2. 定理的证明

下面为了计算方便,对所有的 ,我们令

,我们令

,

, ,

,

,

, ,

,

计 ,

, ,

, ,

, ,这样我们得到

,这样我们得到

。

。

另外,定义一些新的序列

,

, ,

,

,

, 。

。

为了证明定理内容,我们引入下面引理

引理2.1:对于模型(1),我们得到

以及 ,

, 。

。

证明:由Phillips和Magdalinos [6] ,我们知 ,故对所有的

,故对所有的 ,有

,有

, (2)

, (2)

通过简单的计算,我们可以得到

另外,通过公式(2)和 ,我们可以得到

,我们可以得到

以及

以及 。

。

引理2.2:当 无穷大时,我们得到

无穷大时,我们得到

,其中

,其中 ,

,

并且

证明:通过 [7] 中的推论5.5,我们只需要证明:对任意的非零向量 ,有

,有

,对任意的

,对任意的 ,令

,令 ,有

,有 。

。

一方面,因为 是一个独立非同分布随机变量列,通过一些简单的计算可得到

是一个独立非同分布随机变量列,通过一些简单的计算可得到

其中

另一方面,因为当 无穷大时,存在一个足够大的数

无穷大时,存在一个足够大的数 ,有

,有

并且

对任意的 ,我们有

,我们有

因为 ,

, 故有

故有 ,所以我们可以得到

,所以我们可以得到

即有 ,又因为

,又因为 的可积性及

的可积性及 ,所以有

,所以有

,因此我们可以得到Lindeberg条件

,因此我们可以得到Lindeberg条件 ;

;

基于上面两方面的原因,我们可以得到这个引理的证明。

引理2.3:当 无穷大时,我们可以得到

无穷大时,我们可以得到

,

, ,

, ,以及

,以及

,

, 。

。

证明:首先,我们通过Phillip和Magdalions在 [6] 中对公式(10)的证明以及引理2.1可以得到 以及

以及 。

。

其次,通过引理2.1,引理2.2以及 ,我们可以得到

,我们可以得到

另外

易知:

(3)

(3)

(4)

(4)

又因为

故

(5)

(5)

同理可知:

(6)

(6)

结合(3) (4) (5) (6)得:

。

。

最后,易知 。

。

引理2.4:当 无穷大时,我们有

无穷大时,我们有 。

。

证明:由[3] 中(A.14)和(A.23)式,令 ,得到

,得到

; (7)

; (7)

又

, (8)

, (8)

并且

,

,

因此根据(7)式我们可以得到 ,其中

,其中

由引理2.3得 及

及 ,引理得证。

,引理得证。

定理1的证明

由(7) (8)式得, ,

,

其中 。

。

由引理2.1和引理2.3得

(9)

(9)

又经过简单的计算得

, (10)

, (10)

结合(9)(10),定理得证。

致谢

本论文是在我与同学孟娇的合作中完成的。感谢导师给予我们的支持,感谢南京航空航天大学数学系的各位老师给予我们的指导和帮助,感谢各位文献作者的成果给予我们的借鉴。

文章引用

于明明,孟 娇, (2014) 近爆炸性自回归序列中参数估计量的渐近性质

Asymptotic Properties for the Parameter Estimator in the Near-Explosive Autoregressive Process. 理论数学,06,261-267. doi: 10.12677/PM.2014.46038

参考文献 (References)

- 1. Anderson, T.W. (1959) On asymptotic distributions of estimators of parameters of stochastic difference equations. Annals of Mathematical Statistics, 32, 676-687.

- 2. Zhou, Z.Z. and Lin, Z.Y. (1958) Asymptotic theory for LAD es-timation of moderate deviations from a unit root. Statistics and Probability Letters, 29, 1188-1197.

- 3. Bercu, B. and Proia, F. (2013) A sharp analysis on the asymptotic behavior of the Durbin-Watson statistic for the first-order autore-gressive process. ESAIM: Probability and Statistics, 17, 500-530.

- 4. Chan, N.H. and Wei, C.Z. (1987) Asymptotic inference for nearly nonstationary AR(1) processes. Annals of Statistics, 15, 1050-1063.

- 5. Nabeya, S. and Perron, P. (1994) Local asymptotic distributions related to the AR(1) model with dependent errors. Journal of Econometrics, 62, 229-264.

- 6. Phillips, P.C.B. and Magdalinos, T. (2007) Limit theory for moderate deviations from a unit root. Journal of Econometrics, 136, 115-130.

- 7. Kallenberg, O. (2002) Foundations of modern probability. Springer, Berlin.