Pure Mathematics

Vol.4 No.04(2014), Article

ID:13888,6

pages

DOI:10.12677/PM.2014.44022

The Gerber-Shiu Discounted Penalty Function for the Risk Model with Phase-Type Inter Claim Times

School of Mathematics and Computer Science, Shanxi Normal University, Linfen

Email: xiaojuxia2426@126.com

Copyright © 2014 by author and Hans Publishers Inc.

This work is licensed under the Creative Commons Attribution International License (CC BY).

http://creativecommons.org/licenses/by/4.0/

Received: Jun. 12th, 2014; revised: Jul. 10th, 2014; accepted: Jul. 17th, 2014

ABSTRACT

Research in the phase-type distribution has an important influence for the research of other distributions on the positive real axis. It considers the risk model with the phase-type inter-claim times and for constant interest, it first derives the integral-differential equation satisfied by the Gerber-Shiu discounted penalty function. Then through a series of deriving, it obtains the volterra integral equation in a form of matrix. It gets a method of solving the Gerber-Shiu expected penalty function.

Keywords

Phase-Type Inter-Claim Times, Constant, Integral Function, Differential Equation, Volterra

带常利率的时间间隔为相位的Gerber-Shiu折现罚金函数

肖菊霞

山西师范大学数学与计算机科学学院,临汾

Email: xiaojuxia2426@126.com

收稿日期:2014年6月12日;修回日期:2014年7月10日;录用日期:2014年7月17日

摘 要

相位分布的研究在研究正半轴的其他分布中起着重要作用。考虑带常利率的时间间隔为相位分布的更新风险模型。首先推导出Gerber-Shiu期望折现罚金函数满足的积分微分方程,然后经过一系列的推导过程得到Volterra形式的矩阵积分方程,从而得到Gerber-Shiu期望折现罚金函数的一种解法。

关键词

时间间隔为相位分布,常利率,积分方程,微分方程,Volterra

1. 引言

带常利率的更新风险模型, 时刻资产余额

时刻资产余额 的微分方程形式为

的微分方程形式为

,

,

其中常数 表示初始准备金,常数

表示初始准备金,常数 表示保费率,常数

表示保费率,常数 表示常利息力。

表示常利息力。 表示

表示 时刻为止的总索赔额,更新过程

时刻为止的总索赔额,更新过程 表示

表示 时刻为止的总索赔次数;索赔额

时刻为止的总索赔次数;索赔额 是分布为

是分布为 ,密度为

,密度为 的独立同分布随机变量;

的独立同分布随机变量; 表示第

表示第 次索赔发生时刻,其中

次索赔发生时刻,其中 ;索赔时间间隔

;索赔时间间隔 是独立同分布的正随机变量,其分布函数

是独立同分布的正随机变量,其分布函数 ,密度函数

,密度函数 。则

。则 。

。

当初始余额为 时,破产时刻

时,破产时刻 定义为:

定义为:

若 ,则表示破产没有发生;若有破产发生,则破产前瞬间资产余额为

,则表示破产没有发生;若有破产发生,则破产前瞬间资产余额为 ,破产时赤字为

,破产时赤字为 ,期望折现函数是破产前瞬间资产余额和破产时赤字的期望折现,当初始余额为

,期望折现函数是破产前瞬间资产余额和破产时赤字的期望折现,当初始余额为 时,定义为:

时,定义为:

其中 是破产前瞬间资产余额和破产时赤字的非负罚金函数,折现因子

是破产前瞬间资产余额和破产时赤字的非负罚金函数,折现因子 是非负参数,

是非负参数, 是示性函数。

是示性函数。

相位分布是在风险理论中最常见的分布之一,近年来人们越来越关注时间间隔为为相位分布的Sparre Andersen模型。例如[Albrecher and Boxma] (2005)通过Laplace-Stieltjes变换分析折现罚金函数,[Dickson and Drekic] (2004), [Jiandong Ren] (2008)[1] 考虑了研究了破产前瞬间资产余额和破产时赤字的联合分布函数,又如[Mogens Bladt] (2005)[2] 研究了相位分布的应用。

对Gerber-Shiu折现罚金函数的研究是破产理论主要研究的问题之一。对此问题的研究始于[Gerber and Shiu] (1998)[3] ; [Dickson and Hipp] (1998), [Lin] (2003)研究了时间间隔为Erlang (2), [Rong Wu, Yuhua Lu, and Ying Fang] (2007)[4] 研究了时间间隔为相位分布。

常利息力更新风险模型也是现代风险理论研究的重要方面, 许多人都做过这方面的工作。例如[Sundt and Teugels] (1997), [Yang and Zhang] (1997), [Cai] (2002)[5] , [Cardoso and Waters] (2003)。

本文考虑带常利率的时间间隔为相位分布的更新风险模型。首先推导出Gerber-Shiu期望折现罚金函数满足的积分微分方程,然后经过一系列的推导过程得到Volterra形式的矩阵积分方程,从而得到Gerber-Shiu期望折现罚金函数的一种解法。

2. 相位分布简介

假定索赔时间间隔的分布 是参数为

是参数为 的相位分布,连续时间马氏链

的相位分布,连续时间马氏链 有

有 个暂态

个暂态 和一个吸收态

和一个吸收态 。其中

。其中 ,

, ,

, ,

, ,

, 是从暂态

是从暂态 跳到吸收态的密度,

跳到吸收态的密度, ,

, 。

。 是从暂态

是从暂态 跳到暂态

跳到暂态 的密度,

的密度, 是初始分布概率,其中

是初始分布概率,其中 ,

, ,

, 。

。

对 ,

, 是初值为

是初值为 ,初始状态

,初始状态 的期望罚金折现函数,定义为:

的期望罚金折现函数,定义为:

(1)

(1)

若记

(2)

(2)

则期望折现罚金函数 可由下式给出:

可由下式给出:

(3)

(3)

3. 主要结论

定理2.1 对任意的

证明:考虑在足够小的时间 内,由相位分布的性质,在此时间段内最多发生一次状态改变(暂态之间变化)或发生一次索赔,而且状态改变与索赔不可能同时发生,故

内,由相位分布的性质,在此时间段内最多发生一次状态改变(暂态之间变化)或发生一次索赔,而且状态改变与索赔不可能同时发生,故 可在下面三种情况下取得1)在时间

可在下面三种情况下取得1)在时间 内没有发生索赔及状态改变;2)在时间

内没有发生索赔及状态改变;2)在时间 内没有发生索赔但发生状态改变;3)在时间

内没有发生索赔但发生状态改变;3)在时间 内发生

内发生

一次索赔,索赔后可能导致破产也可能没有破产,当索赔额 时,表示没有破产,当

时,表示没有破产,当 时,表示破产发生。

时,表示破产发生。

由以上及(1)式可知:

(4)

(4)

因为

所以(4)式为

(5)

(5)

移项整理(5)且等式两端同除 得:

得:

(6)

(6)

在(6)中,令 ,且由

,且由

可得:

推论2.1 对任意的

(7)

(7)

其中 。

。

证明:由(2)(4)及相位初始分布的性质 直接推出。

直接推出。

定理2.2 对任意的

(8)

(8)

其中 。

。

证明:(7)式两边同乘 ,得到

,得到

整理得

(9)

(9)

用 替换

替换 (9)式变为

(9)式变为

(10)

(10)

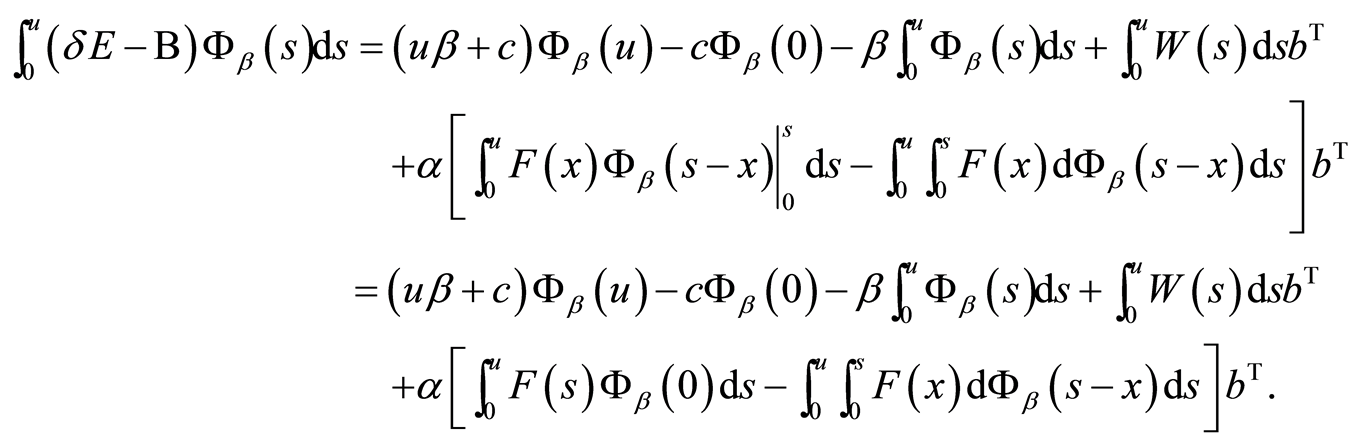

(10)式两端对变量s作积分,有

若记E为n阶单位矩阵,由分部积分法及 ,得

,得

(11)

(11)

而

故而(11)式为

故而

引理2.1

若 是向量函数,且

是向量函数,且 是Volterra核矩阵,即

是Volterra核矩阵,即

其中 是

是 上的

上的 可积函数,则对任意的

可积函数,则对任意的 ,

, 的解可以表示为:

的解可以表示为:

其中

是迭核,按方阵的乘积处理。

是迭核,按方阵的乘积处理。

注:引自参考文献[6] 。

定理2.3 对任意的

(12)

(12)

其中

以方阵的乘积处理,

以方阵的乘积处理, 为

为 阶单位阵。

阶单位阵。

证明:(8)式为Volterra积分方程组形式

由于 可微,故

可微,故 是

是

核矩阵,从而由引理2.1可得结论。

核矩阵,从而由引理2.1可得结论。

4. 结论与建议

由(12)可知,只需求出 便可得出

便可得出 ,再由

,再由 可求出期望惩罚函数

可求出期望惩罚函数 。

。

在定理2.2中令 ,可得Volterra积分方程组形式

,可得Volterra积分方程组形式

在定理2.3中取 ,则有

,则有

其中

以方阵的乘积处理,

以方阵的乘积处理, 为

为 阶单位阵。

阶单位阵。

由以上推导可知,只要求出 ,就可求出

,就可求出 ,进而可求出

,进而可求出 。

。

参考文献 (References)

- Ren, J.D. (2008) The discounted joint distribution of surplus prior to ruin and the deficit at ruin in a sparre andersen model. North American Actuarial Journal, 11, 128-136.

- Bladt, M. (2005) A review on phase-type distributions and their use in risk theory. Astin Bulletin, 35, 145-161.

- Gerber, H.U. and Shiu, E.S.W. (1998) On the time value of ruin. North American Actuarial Journal, 2, 48-72.

- Wu, R., Lu, Y.H. and Fang, Y. (2007) On the Gerber-Shiu discounted penalty function for the ordinary renewal risk model with constant interest. North American Actuarial Journal, 11, 135.

- Cai, J. and Dickson, D.C.M. (2002) On the expected discounted penalty function at ruin of a surplus process with interest. Insurance: Mathematics and Economics, 30, 389-404.

- 《现代应用数学手册》编委会 (2006) 现代应用数学手册, 分析与方程卷. 清华大学出版社, 北京, 921-963.